Insurtech might not be the flashiest sector at first glance, but it's undergoing one of the most exciting transformations in Europe right now. At Endeit Capital, we’re excited by how technology, regulatory shifts, and changing consumer habits are sparking fresh, innovative trends in an industry ripe for modernization, even though Insurtech has been around for a while. First, let's dive into the concept of Insurtech, why we got our eye on it, and what trends to watch.

Written by: Jeroen van der Does de Willebois.

Insurtech (short for insurance technology) refers to the use of modern digital solutions to enhance, complement, or even disrupt traditional insurance models. At Endeit, we see these shifts happening in real time. The rapid deployment of API integrations, AI-powered underwriting, and the rise of on-demand insurance models are radically transforming how we engage with insurance. From instant quotes to near real-time claims payouts, customers now expect transparency, speed, and personalization—something legacy insurers are struggling to provide.

At present, traditional insurers often struggle with outdated (tech) infrastructure, whereas insurtech firms are agile, tech-native, and laser-focused on solving specific pain points within the insurance value chain. Key areas they target include:

Today, insurtechs are not just digital upstarts, —they’ve been around for more than a decade and have matured into key players driving change in a historically risk-averse industry. By building digital-first, customer-centric solutions, insurtechs are now forcing traditional players to adapt—or risk being left behind.

Insurtechs typically play one of three roles:

The result? Faster innovation cycles, lower costs, and new products that better match today’s dynamic risk landscape. By doing so, they help reduce paperwork, speed up quote and claim processes, and offer personalized products (such as usage-based or on-demand insurance) that traditional insurers have struggled to provide.

While consumer-facing apps steal the spotlight, the real backbone of this transformation is built by B2B enablers. These companies, now responsible for more than 60 % of global insurtech deals in Q1 2025 (Global InsurTech Report Q1 2025), are modernizing legacy systems with advanced analytics, smooth API integrations, and cloud-native solutions.

They provide:

The impact is significant: currently targeting to reduce operational costs by up to 20% while opening up entirely new business models (McKinsey, 2024).

For example Qover delivers a flexible, API-driven embedded insurance solution that integrates directly into digital sales channels. It allows partners to offer tailored coverage—from travel and gig economy policies to personal liability protection—without the need to build complex systems from scratch.

AI is the connective tissue that powers many of the innovations and trends across the insurtech landscape discussed above. Whether it’s tailoring embedded insurance offers in real time, evaluating dynamic risks from emerging threats like cybercrime and climate change, or enabling B2B platforms to launch adaptive products at speed, artificial intelligence sits at the heart of this transformation. Nearly 30% of recent European insurtech funding (The state of InsurTech 2024, Astorya) is fueling AI-powered platforms that, for example, settle claims in minutes rather than weeks, drastically reducing operational costs while fine-tuning risk pricing.

For example, Shift Technology. Their AI-driven platform meticulously analyzes claims data in real time, identifying fraud patterns and automating routine claim verifications. This not only accelerates the claims process but also significantly reduces manual errors and fraud-related losses.

What does the future look like? Let’s dive into some of the biggest trends.

At the moment, embedded insurance is the hottest trend on the block. Whether booking a flight, renting a car, or buying a smartphone, consumers can now add coverage with a single click. Insurtechs are meeting customers where they already are, slashing customer acquisition costs and tapping into untapped markets. Projections show the European embedded insurance market skyrocketing and growing at double digits next few years. With conversion rates leaping up by 20% compared to traditional methods, it’s proof that seamless integration is the future (Open & Embedded Insurance Observatory, 2024).

For example, Laka. Imagine buying a new e-bike (online). Instead of going to a separate insurer at check-out it includes an offer to insure the bike instantly, with pricing based on actuals riding behavior of people & with payouts happening in hours, which is what Laka offers.

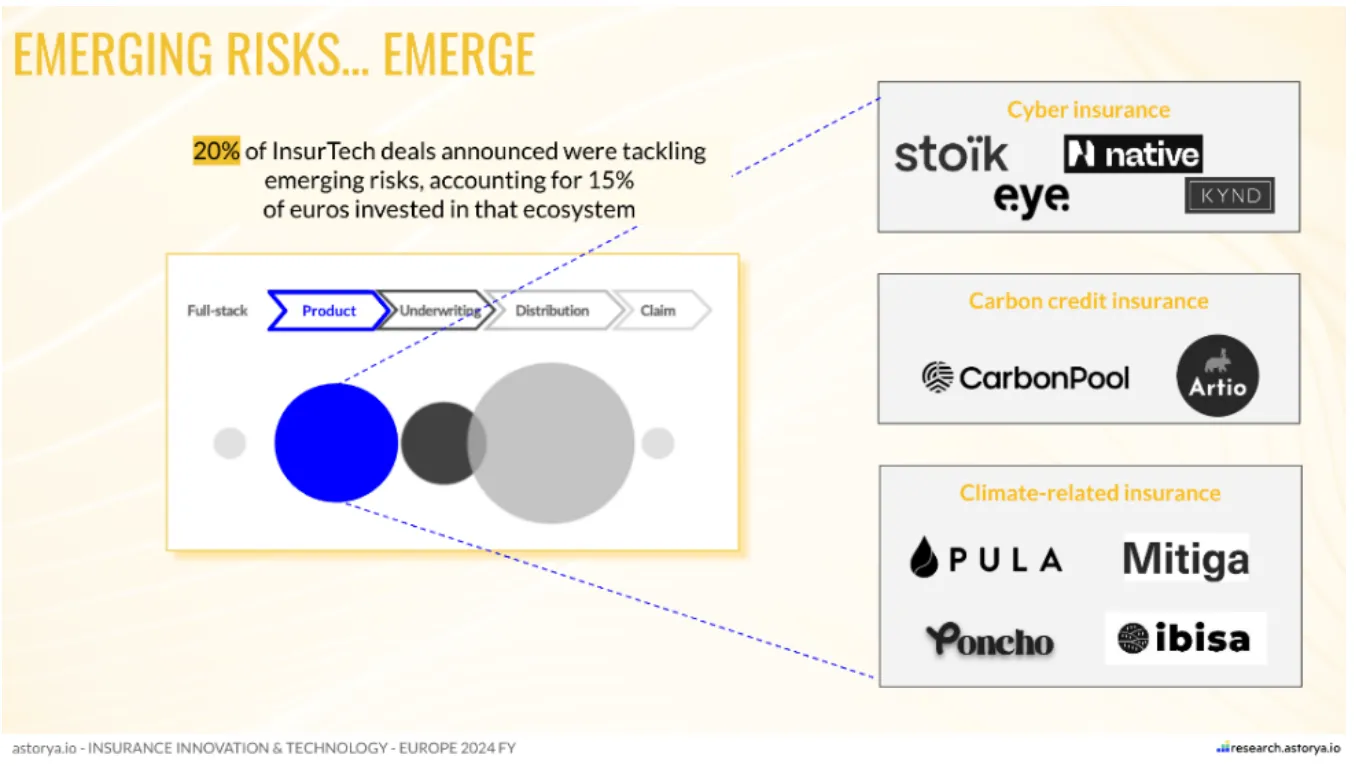

Next, let’s consider what we believe might be the biggest emerging trend of all: emerging risks. We view this as an exciting new trend, as emerging risks can go unrecognized for a long time, until they manifest themselves as serious trend developments or spontaneous risk events. At the moment, the risk environment is evolving faster than most traditional insurance models can keep up with. For example, We’ve observed some of the following emerging risks:

What all emerging risks have in common is that their occurrence probability, loss amount and potential impact are exceedingly difficult to quantify. Not least, because cases of this kind have never happened before, or only rarely. That’s why we need start-ups tackling these new challenges head-on with forward-looking, real-time solutions. These include parametric insurance products that automatically pay out when specific conditions are met, like rainfall thresholds or wind speeds, as well as cyber policies bundled with monitoring tools to detect and prevent breaches. Many are now integrating climate risk data and satellite analytics into underwriting. It’s no surprise, then, that in the past year, around 20% of European insurtech funding has gone toward ventures in these high-impact areas—cutting claims processing times by up to 50% and delivering tailored coverage where traditional insurers fall short (Astorya, 2024).